Illinois politicians have Illinoisans arguing over tax hikes and tax schemes instead of what’s really needed to fix our state – spending reforms. Skyrocketing pension costs are the elephant in the room and yet no one is talking about them.

It’s pension reform that should be on the Nov. 3rd ballot. Reforms could save Illinoisans billions, offsetting the need for more tax hikes. Wirepoints made that case in its recent Chicago Tribune oped.

The need for pension reform is obvious. Illinois pensions are overpromised and overgenerous. Everyone has read about the many perks in the press. State workers retire in their 50s. Contracts across the state hand out end-of-career salary spikes, which boost pensions. Years of unused sick leave can be banked and then turned into cash or bigger pensions. Many workers have their required pension contributions picked up by their employer, meaning taxpayers pay the costs. All of those and more push up lifetime pensions for the average career worker to more than $2 million. And there are many administrators that end up collecting a massive $4 million to $10 million in lifetime benefits.

At Wirepoints, we decided to see just how much of an outlier the state is. We compared Illinois’ pension promises to those of its peer states – the nation’s five largest and Illinois’ neighbors.

We FOIA’d for information and scoured the actuarial reports of each state. We focused on teachers because they are the most comparable group of government workers in the country, and teacher pensions make up nearly 60 percent of Illinois’ pension crisis.

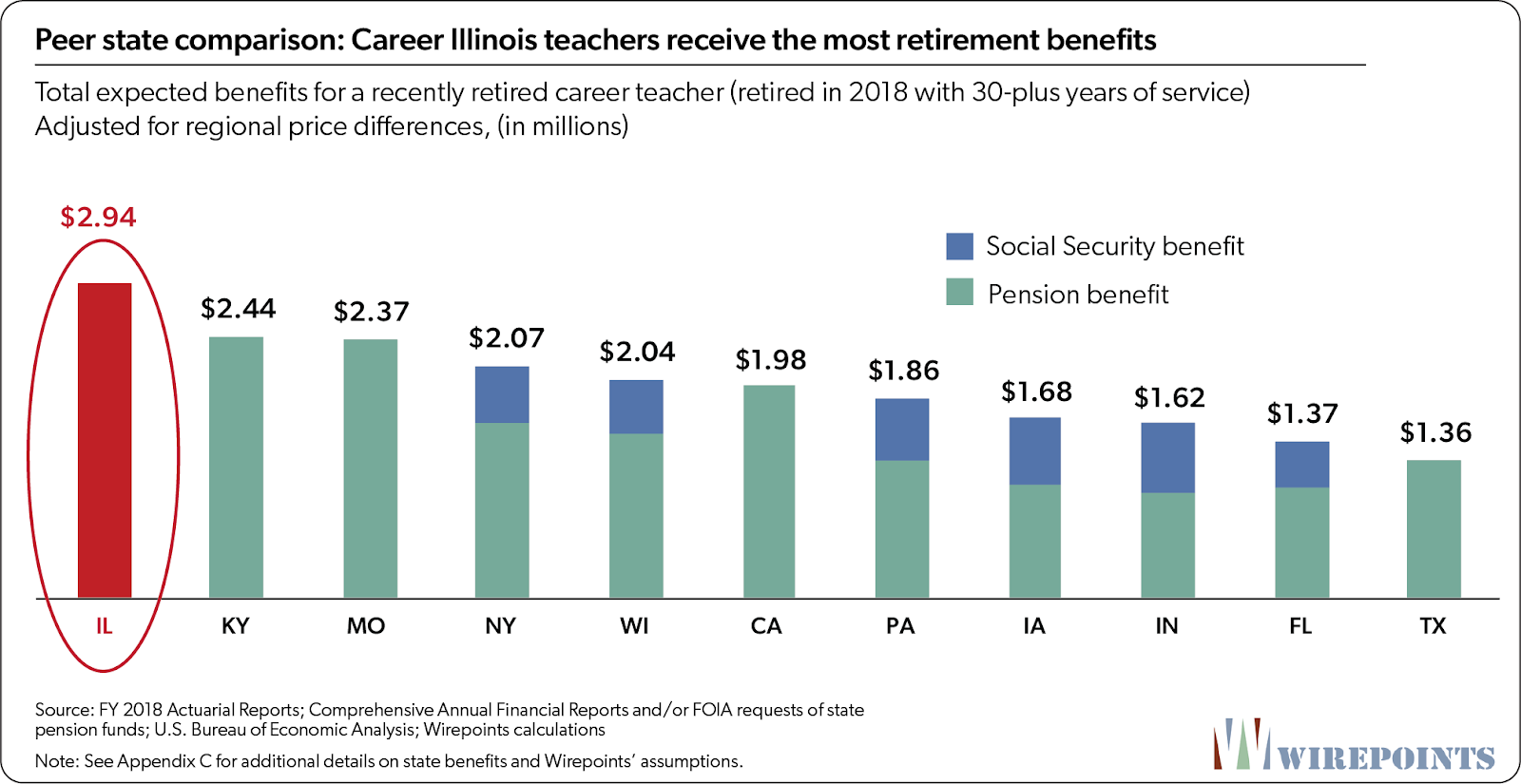

Unsurprisingly, Illinois’ benefits were the biggest. Career teachers - those who work 30-plus years - can expect to collect $2.9 million in benefits. They out-earn colleagues in expensive blue states like California and New York by a large margin, especially after adjusting for regional costs.

Retired teachers in New York get approximately $2.1 million in benefits, while California teachers get $2.0 million. Illinois’ benefits are far bigger than those in states like Indiana ($1.6 million), Florida ($1.4 million) and Texas ($1.4 million).

The above is true even before adjusting for cost differences between states and regions. Illinois is still at the top.

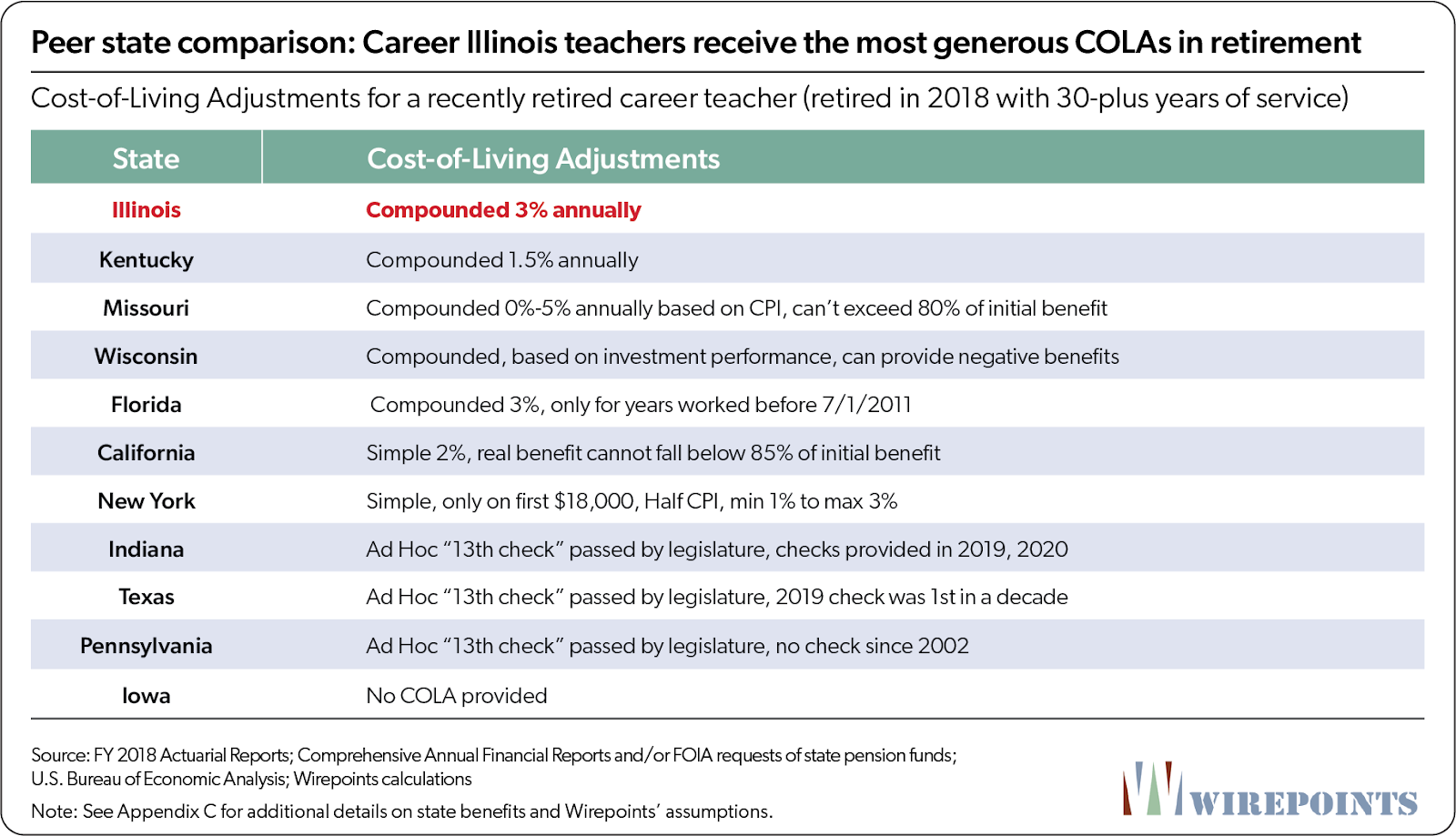

Illinois teachers out-earn their peers because they have the highest Final Average Salaries, the most generous starting benefits, and retire earlier than most other teachers. And the 3 percent annual, automatic, compounded COLA they receive is also the most generous.

We laid out all those details in our special report Illinois Pensions: Overpromised & Overgenerous.

COLAs aren’t automatic in Texas, Pennsylvania, and Indiana. Those states can go for years without granting what’s called a “13th check.” Wisconsin’s COLA varies widely from year to year and can actually go negative when investment returns fall, cutting a teacher’s annual benefits.

Even New York and California don’t come close to offering the benefit Illinois does. California grants a 2 percent simple COLA and New York’s benefit only grants a 1 to 3 percent simple increase on the first $18,000 of a teacher’s pension.

The closest is Kentucky. It grants teachers a 1.5 percent annual compounded COLA. High COLA’s in Kentucky for sure contribute to that state’s woes. The state has some of the worst funded pensions in the country alongside Illinois.

Illinois’ COLAs have a massive impact on how much teachers get. The compounded 3 percent increase doubles a teacher’s annual pension benefit after 25 years, so a teacher with a starting pension of $100,000 in 2020 will receive $203,000 in 2045.

That doubling, for hundreds of thousands of government beneficiaries, is a major contributor to the massive pension debts Illinoisans are on the hook for.

In contrast, Kentucky’s 1.5 percent compounded COLA grows a $100,000 starting pension to $143,000 in 25 years, a 43 percent increase. New York’s COLA benefit boosts a teacher’s $100,000 starting pension to a maximum of $113,000. And Iowa teacher benefits don’t grow at all because the state doesn’t provide any increase.

The data above is clear. No matter how you measure it, Illinois’ teacher benefits outclass those in every peer state. That’s helped drive up total pension promises to a level ordinary Illinoisans can no longer pay for.

That’s the discussion we should be having. How to bring down those costs in a fair way for our retirees, our taxpayers and our most vulnerable who’ve seen core services cut as pension costs balloon.

Instead, politicians are dividing us and making us fight over tax hikes. They are playing us one more time.

To learn more about pension reform, go to Wirepoints’ landing page Pension Solutions. In about a week, we’ll be laying out a baseline reform plan that finally begins an end to Illinois’ perpetual crisis. It’s ambitious, but it’s what Illinoisans need.